Summary:**Autonomous Vehicle Edge Compute Rig Market Poised for Massive Growth to $9.1B by 2030***Introducti

referrerpolicy="no-referrer"

referrerpolicy="no-referrer"

style="max-width:100%;height:auto;display:block;margin:0 auto;">

**Autonomous Vehicle Edge Compute Rig Market Poised for Massive Growth to $9.1B by 2030**

*Introduction*

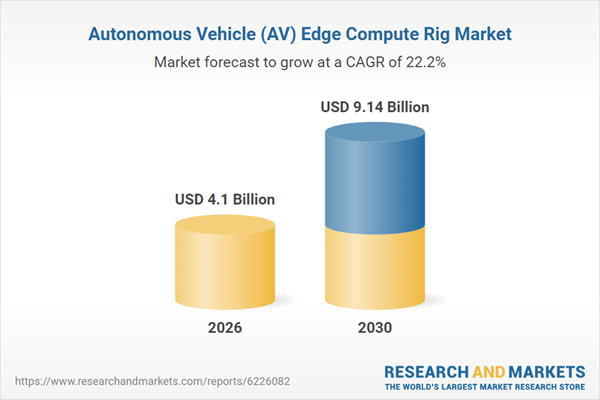

The race to deploy fully self‑driving cars is accelerating, and the hardware that makes split‑second decisions possible is becoming a hot commodity. Analysts now forecast the autonomous vehicle edge compute rig market to swell from roughly $2.3 billion in 2023 to a staggering $9.1 billion by 2030, driven by surging demand for real‑time data processing, tighter AI integration, and the rollout of 5G networks. This rapid expansion promises new opportunities for chip makers, system integrators, and automotive OEMs alike.

*Key Developments*

Recent months have seen several milestones that underline the market’s momentum. NVIDIA unveiled its next‑generation DRIVE Orin‑2 platform, promising up to 1,000 TOPS of AI performance while cutting power consumption by 30 %. Simultaneously, Qualcomm announced a partnership with a leading European EV manufacturer to embed its Snapdragon Ride Flex SoC into production vehicles slated for 2025. On the connectivity front, Ericsson and Nokia have begun piloting private 5G slices at test tracks in Michigan and Bavaria, demonstrating latency under 5 milliseconds—critical for edge‑based perception pipelines. These advances are not isolated; they reflect a broader trend where semiconductor firms, telecom providers, and automakers are co‑engineering solutions that meet the stringent safety and performance thresholds of Level 4 autonomy.

*Industry Analysis*

Several forces are converging to fuel this growth. First, the proliferation of advanced driver‑assistance systems (ADAS) is creating a baseline demand for onboard compute that can handle sensor fusion, object detection, and path planning in real time. Second, the global shift toward electric vehicles (EVs) is freeing up thermal and power budgets that manufacturers can redirect toward more powerful edge processors. Third, cloud‑to‑edge continuities are maturing; OEMs now offload non‑critical map updates and fleet‑learning tasks